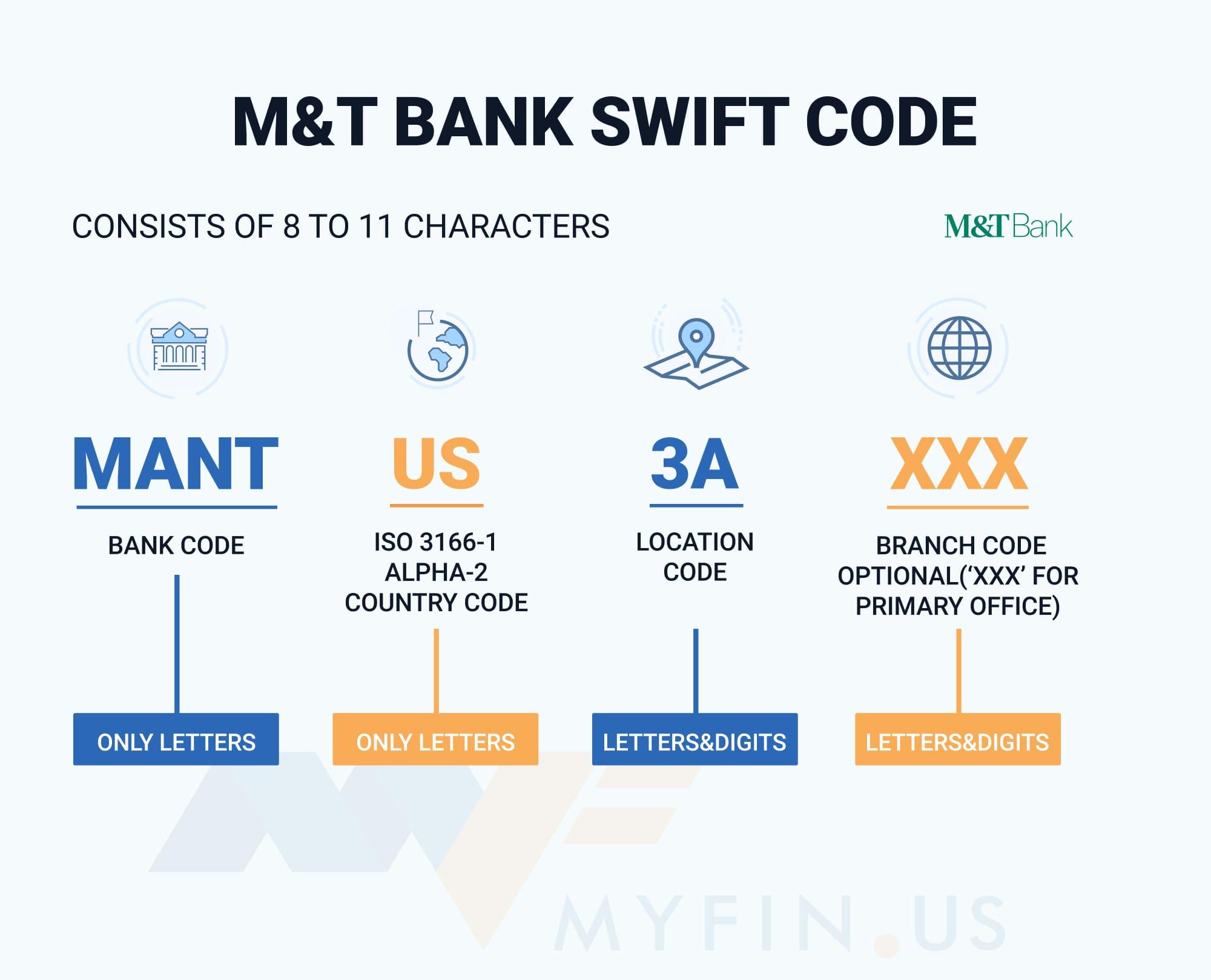

This process involves initiating a transfer of funds using a unique code provided by a financial institution, typically First Bank. This code is often used for transactions between accounts held at the same institution. The code may be generated in response to a request for a specific transaction, or may be part of a pre-authorized or scheduled transfer. Examples include transferring money between savings and checking accounts, or initiating a payment to a designated payee within the institution's system.

Such transfers offer speed and convenience, often circumventing the need for manual entry of account details for each transaction. This streamlined approach can reduce the risk of errors associated with manual input, especially for routine payments. The security of these codes is critical, and robust authentication procedures are essential to prevent unauthorized access and fraudulent activity. The efficiency and security offered by this method are important factors in the overall banking experience. This practice, when done correctly, contributes to greater financial transaction security.

This method of fund transfer is a key component of modern banking. Moving forward, the article will examine the security measures employed in this type of transaction, the typical steps involved, and the differing rates for such transactions across various First Bank products.

First Bank Code Transfer

Understanding the essential components of First Bank code transfer is crucial for secure and efficient financial transactions. This process relies on a combination of technological and security measures.

- Authentication

- Security protocols

- Account access

- Transaction initiation

- Funds availability

- Code generation

- Transaction confirmation

- Error handling

These aspects are interconnected, forming a system that protects funds. Authentication mechanisms, like passwords or security tokens, are the first line of defense. Robust security protocols, including encryption, are essential for safe code generation and transfer. Initiating a transaction requires proper account access. Funds availability needs verification before a code can be used. Codes should be generated in a secure manner. Confirmation is needed to ensure the transfer is completed successfully. A robust system should also account for possible errors. For example, if a code is invalid, the system should provide clear guidance. These safeguards ensure secure and reliable financial transactions. Through these steps, First Bank strives to provide its customers with a dependable and secure banking experience.

1. Authentication

Authentication is paramount to secure code-based fund transfers at First Bank. The integrity of the transfer process hinges on verifying the user's identity. Without robust authentication, unauthorized access becomes a significant risk, potentially leading to fraudulent transactions. A compromised system allows malicious actors to initiate transfers without legitimate authorization.

Multiple authentication methods are employed, such as security questions and responses, multi-factor authentication, or biometric verification. These methods help to differentiate between legitimate users and unauthorized individuals, mitigating the threat of fraudulent activity. The system verifies not only the user's identity but also ensures only authorized actions can be initiated. Examples include verifying the user's credentials associated with a registered account. In essence, strong authentication safeguards funds and protects the institutions reputation. This is crucial for maintaining user trust and preventing financial loss. Failure to properly authenticate a user can open the system to security breaches, including but not limited to code-based fraudulent transfers. This understanding underlines the crucial role of secure authentication for robust financial transactions.

A fundamental understanding of authentication within the context of First Bank code transfers is essential. A secure authentication system forms the cornerstone of financial transactions, enabling reliable and efficient processes. This understanding extends beyond the individual transaction, impacting overall user confidence and the institution's financial security. Strengthening authentication practices is a continuous effort crucial for maintaining security against evolving threats in the financial sector. Furthermore, this approach reinforces adherence to industry best practices for secure fund transfers and safeguards customer assets.

2. Security Protocols

Robust security protocols are fundamental to the integrity of code-based fund transfers at First Bank. These protocols form the foundation of trust, ensuring the security and reliability of transactions. Their effectiveness directly impacts the safety of funds and the prevention of unauthorized access.

- Encryption

Encryption techniques, such as advanced cryptography, are crucial. Data transmitted during code-based transfers is encrypted, rendering it unreadable to unauthorized parties. This protection safeguards sensitive information from interception or alteration during transit. Examples include using encryption to protect code generation and transmission between systems.

- Authentication Mechanisms

Beyond simple usernames and passwords, multifaceted authentication methods are used to verify user identity. These measures include multi-factor authentication, employing multiple verification steps to confirm the user's authorization. This enhances the protection against unauthorized access by requiring more than just a password, deterring malicious actors who may gain password access but lack additional factors.

- Secure Communication Channels

Code transfer relies on secure channels to facilitate communication between systems. This involves using protocols that ensure data integrity and confidentiality during the transfer process. Employing secure communication channels prevents malicious actors from intercepting or modifying transfer instructions.

- Regular Security Audits and Updates

Security protocols are not static. Regular audits and updates are essential. These ensure protocols remain effective against emerging threats and vulnerabilities. Continual evaluation and updates to the system's security mechanisms address new security threats and potential vulnerabilities, preserving the integrity of the fund transfer process.

These security protocols, when properly implemented, contribute significantly to the overall safety and reliability of code-based fund transfers at First Bank. By adhering to robust and updated security measures, the institution safeguards customer assets, protecting against financial losses and maintaining customer trust.

3. Account Access

Account access is a critical component of any code-based fund transfer process, including those at First Bank. Proper account access control is essential to ensuring only authorized individuals can initiate transfers. The security and integrity of the entire system depend on the reliability and effectiveness of these access mechanisms.

- Verification Methods

Various methods validate the identity of the user attempting to access an account and initiate a transfer. These methods include usernames and passwords, security questions, multi-factor authentication (MFA) employing one-time passwords or biometric verification. The sophistication of verification methods directly correlates with the level of security. Robust multi-factor authentication significantly reduces the risk of unauthorized access. Implementing these methods strengthens the security of the transfer process, safeguarding against fraudulent activity.

- Account Security Policies

Clear policies outline the procedures for accessing accounts and initiating transfers. These policies detail the steps necessary to verify identity, the permissible actions within the system, and the limitations on account access. Adherence to these policies is crucial for maintaining security. For instance, policies might restrict access during certain hours, or require prior notification for large transfers. These policies form a cornerstone of account security within the broader code transfer system.

- Access Control Levels

Implementing varying levels of access control can differentiate user privileges. Different users might have different levels of access, such as viewing account balances or initiating transfers. This structure limits potential damage should an account be compromised. For example, a user might only be able to check their account balance, while a different user is authorized to initiate or receive transfers. Differentiating access levels is essential for ensuring granular control over accounts within the transfer system, minimizing potential risks and safeguarding assets.

- Account Lockout Procedures

Account lockout mechanisms are crucial for preventing unauthorized access attempts. Excessive or suspicious login attempts can trigger account lockouts, temporarily restricting access. This approach, if appropriately implemented, can deter malicious actors. These procedures help protect accounts from breaches by temporarily suspending access after a series of failed login attempts. The effectiveness of lockout procedures directly contributes to the overall security of the transfer process.

Effective account access management is an integral part of secure code-based fund transfers. By implementing robust verification, clear policies, appropriate access control levels, and efficient lockout procedures, First Bank, and other institutions, can mitigate risks associated with unauthorized access and ensure the reliability of the fund transfer process. Strong account access controls safeguard customer assets and maintain public trust in the financial system.

4. Transaction Initiation

Transaction initiation forms a critical link in the process of code-based fund transfers at First Bank. It encompasses the initial steps required to execute a transfer, from the user's request to the system's confirmation of the transaction. A smooth and secure transaction initiation process directly impacts the integrity and efficiency of fund transfers.

- Authorization and Validation

The initiation phase begins with user authorization. This validation ensures only permitted users can initiate transfers, mitigating the risk of unauthorized transactions. It involves verifying user credentials, often employing multi-factor authentication to enhance security. For instance, a user might need to enter a unique code from a mobile device in addition to their password. This layered approach prevents fraudulent activity by demanding multiple forms of verification, preventing unauthorized access.

- Code Generation and Verification

The system generates a unique code specific to the transfer. This code is crucial for the subsequent transfer execution. Critical validation checks are performed. These checks include verifying the availability of funds in the source account and ensuring the destination details are correct. The validity of the code is vital to avoid errors and ensure the funds are sent to the intended recipient. Examples include confirming account numbers and verifying sufficient funds. The integrity of this process safeguards against errors and prevents unauthorized or incorrect transfers.

- Transaction Logging and Record Keeping

Detailed records are maintained for every transaction initiation. These logs contain information like the initiating user, the date and time of initiation, the amount transferred, the destination account details, and confirmation codes. This meticulous record-keeping is essential for tracking and resolving any issues that may arise. These logs provide a historical trail, enabling the tracing of any discrepancies or disputes. This detailed record-keeping is crucial for regulatory compliance and internal audits.

- System Integration and Interoperability

Transaction initiation seamlessly integrates with other bank systems. This integration allows for seamless communication between different banking departments and ensures the transfer process is properly routed within First Bank's infrastructure. Integration with other banks or financial institutions is necessary for interoperability in transactions involving multiple entities. This ensures smooth communication and processing between various elements within the banking system and, in some cases, with external institutions.

These facets of transaction initiation are fundamental to the efficient and secure execution of code-based fund transfers at First Bank. Their precise functioning ensures the integrity of each transaction, safeguarding funds, and upholding the institution's reputation for reliable financial services. The reliability of the entire process rests heavily on the secure and accurate execution of these initial steps.

5. Funds Availability

Funds availability is a critical element in the First Bank code transfer process. It directly impacts the successful execution of a transfer, ensuring sufficient funds are present in the source account before initiating a transaction. Without verification of funds availability, the bank risks processing unauthorized or invalid transfers.

- Verification Procedures

Robust verification procedures are employed to ascertain the sufficiency of funds. These procedures encompass various techniques to validate account balances. Real-world examples include real-time balance inquiries, verifying sufficient funds, and account status checks. Accurate account balance information, consistent with the source account, is vital. Failures in these procedures can result in failed transactions.

- Real-Time Monitoring

Real-time monitoring systems play a crucial role. Continuous checks and updates ensure the availability of sufficient funds. Examples include immediate updates to balances after deposits and deductions, such as withdrawals, or pending transactions. These mechanisms mitigate the risk of issuing codes when insufficient funds exist. Real-time monitoring allows for immediate identification and prevention of transfers that exceed available balances.

- System Integration and Synchronization

The system synchronizes fund availability information across different components. This ensures consistent and accurate data. Examples include synchronizing account balances across various banking platforms. This cohesive data management ensures that the funds availability figures presented for code generation and transfer initiation are consistent with the bank's actual records. Maintaining synchronization is essential for the integrity and security of transactions.

- Transaction Sequencing and Prioritization

Managing and prioritizing transactions is essential when multiple requests simultaneously affect funds. This process, similar to scheduling in an operational system, aims to ensure each transfer is appropriately handled, preventing overdraft situations or conflicts. Examples include prioritizing recurring payments or automated transactions in relation to other transfer requests. Efficient transaction sequencing protects against issues with insufficient funds, preventing failed transfers due to concurrent requests and ensuring fair transaction processing.

Funds availability, therefore, is more than just a simple check. It's a sophisticated process, deeply integrated within the First Bank code transfer system. Precise and timely validation of funds availability, coupled with robust monitoring systems and consistent data synchronization, underpins the security and reliability of every code transfer, contributing to a smooth and secure financial experience. The seamless operation of the funds availability system contributes significantly to the overall efficiency and stability of First Bank's code transfer services.

6. Code Generation

Code generation is a fundamental component of First Bank's code transfer system. It's the process of creating a unique, time-sensitive code used to authorize specific fund transfers. This code acts as a critical link in the chain, securing transactions and preventing unauthorized access. The code's unique nature is essential; it allows for a secure and reliable method for executing transfers.

The significance of code generation stems from its role in maintaining the security of financial transactions. A well-designed code generation system incorporates various factors to ensure the code's integrity and validity. These factors include incorporating a timestamp, a unique identifier tied to the transaction, and cryptographic hashing. The complexity of the code generation algorithm directly affects the system's vulnerability to unauthorized manipulation. A secure code acts as an authentication token, providing a verifiable link between a user and the transaction. The use of a complex algorithm helps deter attempts to replicate or forge codes, ensuring only authorized transfers are processed. For instance, a sophisticated code generation algorithm incorporating time-dependent values prevents replay attacks where a previously generated code is reused for a fraudulent transfer.

Understanding the process of code generation is essential for comprehending the safety and efficiency of code-based transfers. Without secure code generation, the integrity of the entire transfer system is compromised. This lack of security could expose the bank and its customers to significant financial risks. A robust code generation system is an essential line of defense in preventing fraudulent activities, ensuring that only legitimate transactions are executed. This understanding also has broader implications, informing broader security practices related to financial transactions and underscores the need for robust security measures in modern financial systems. The effectiveness of the code generation algorithm directly relates to the system's overall security, emphasizing the importance of technical proficiency and best practices within the financial industry.

7. Transaction Confirmation

Transaction confirmation plays a critical role in the security and integrity of code-based fund transfers at First Bank. It's the final step in the process, validating that the transfer has occurred as intended. The confirmation process serves to verify that the designated funds have been successfully transferred to the intended account. Without robust confirmation procedures, discrepancies and disputes could arise, undermining the reliability of the system.

Confirmation mechanisms must address the crucial need for both immediate feedback to the user and a verifiable record for the bank. Real-world examples illustrate the importance of this step: a user initiates a transfer, receives a confirmation code, and then confirms the transaction. This confirms the transfer has occurred as intended. Failure to receive confirmation could lead to anxiety and delays, and ultimately cause distrust if the transaction doesn't occur. This confirmation mitigates any potential errors or fraudulent activity. Further, the confirmation process establishes an auditable trail, essential for resolving disputes, especially if discrepancies arise. An accurate record of the transaction is vital for regulatory compliance and internal audits.

The practical significance of understanding transaction confirmation in code-based transfers is profound. It ensures that users have confidence in the system's reliability, reduces the risk of errors or disputes, and allows for efficient reconciliation of accounts. A streamlined, secure confirmation process is crucial for building and maintaining customer trust in financial institutions. Effective communication of confirmation status, through clear notifications and transaction summaries, can improve the user experience and minimize confusion.

8. Error Handling

Effective error handling is integral to the robustness and reliability of First Bank's code transfer system. Errors can arise at various stages of the process, from issues with user input to problems within the bank's internal systems. Appropriate error handling mechanisms are essential to gracefully manage these issues and prevent disruptions to the overall transfer process. A well-designed error-handling system must provide clear, actionable feedback to the user, and simultaneously maintain the integrity of the bank's operations.

Consider a scenario where a user inputs an incorrect code. Without proper error handling, the system might freeze, leading to user frustration and potentially loss of trust. A well-designed system, however, would identify this input error, alert the user with an informative message ("Invalid code. Please try again."), and prevent further processing until the correct code is entered. This proactive approach avoids unnecessary complications and maintains the user's confidence in the system. Furthermore, comprehensive error handling enables the bank to identify and address systemic issues, allowing for prompt resolution and preventing potential security breaches. This crucial aspect is vital for preventing cascading effects. For instance, if a database error occurs, the system should not fail catastrophically; instead, it should report the error, preventing further damage and guiding the institution towards fixing the root cause.

The practical significance of understanding error handling in code transfer systems lies in its ability to safeguard financial integrity and maintain user trust. A system with robust error handling is more resilient, minimizing potential losses associated with system failures or user mistakes. This reliability fosters a positive user experience and reinforces the institution's commitment to secure financial transactions. In summary, accurate and timely error handling is critical to preventing issues, maintaining system stability, and upholding a high standard of service in code-based fund transfers. Furthermore, proactive identification of issues by the error handling process allows for timely maintenance and prevents larger, more complicated problems in the future.

Frequently Asked Questions about First Bank Code Transfers

This section addresses common questions regarding First Bank's code transfer process. Understanding these frequently asked questions can enhance the user experience and ensure secure transactions.

Question 1: What is a First Bank code transfer?

A First Bank code transfer is a secure method for initiating funds transfers between accounts within the First Bank system. A unique code, generated by the system, authorizes the transaction, replacing manual entry of account details. This method offers increased security and efficiency.

Question 2: How do I generate a transfer code?

The specific process for generating a transfer code varies based on the chosen transfer method within the First Bank platform. Generally, users access their accounts through designated online platforms or mobile applications. Following the instructions provided by First Bank, the user initiates the transfer and receives the unique code required for completion.

Question 3: What security measures protect my transfer code?

First Bank employs robust security protocols to protect transfer codes. These include encryption, multi-factor authentication, and secure communication channels. These measures significantly reduce the risk of unauthorized access and fraudulent activities.

Question 4: What information do I need to initiate a code transfer?

Users typically need their First Bank login credentials, the recipient account information, and the amount being transferred. The specific information requirements may vary, depending on the type of transfer being initiated.

Question 5: How can I ensure my transfer is completed successfully?

Confirming the transfer code, checking transaction history within the platform, and noting confirmation messages are vital. The user should monitor the transaction status until the transfer is completed and funds are credited to the recipient account.

Question 6: What should I do if I encounter an error during a transfer?

If an error occurs during a transfer, users should carefully review the error message. Contacting First Bank's customer support or reviewing the platform's help resources is recommended for resolving the issue. Users should prioritize secure transactions by adhering to provided guidelines for error resolution.

Understanding these FAQs is essential for a successful and secure code transfer experience with First Bank. The bank remains committed to providing a safe and efficient platform for all transactions.

Moving forward, the next section will delve into the practical applications of code transfers and examine the various types of transfers available within the First Bank system.

Tips for Secure First Bank Code Transfers

Effective utilization of First Bank's code transfer system hinges on adherence to established security protocols. This section provides practical advice to enhance the safety and efficiency of these transactions.

Tip 1: Verify Code Authenticity. Never share transfer codes with anyone. Always ensure the code displayed on the First Bank platform aligns with the intended transaction. Verify the code's origin before initiating any transfer.

Tip 2: Maintain Strong Passwords. Utilize unique and complex passwords for accounts and mobile applications linked to First Bank. Regularly update these credentials. Consider multi-factor authentication to bolster security.

Tip 3: Monitor Account Activity. Actively review account statements and transaction histories regularly. Rapidly report any discrepancies or unauthorized activity to prevent financial loss.

Tip 4: Secure Network Usage. Execute code transfers only on trusted and secured networks. Avoid public Wi-Fi for sensitive financial transactions. Employ VPNs when necessary.

Tip 5: Be Cautious of Phishing Attempts. Exercise vigilance concerning unsolicited requests for personal information or transfer codes. Verify the legitimacy of all communication before responding.

Tip 6: Enable Two-Factor Authentication (2FA). Implementing 2FA adds an extra layer of security. This often involves receiving a one-time code via SMS or authenticator app. Employing 2FA enhances the protection of accounts and prevents unauthorized access.

Tip 7: Keep Software Updated. Ensure all software, including banking applications and operating systems, is updated to the latest versions. These updates frequently address security vulnerabilities.

Tip 8: Report Suspicious Activity Immediately. Any unusual or suspicious activity detected, such as unexpected transfers or login attempts, must be reported promptly to First Bank's customer support. Swift action minimizes potential losses.

Adherence to these tips reinforces security measures and promotes a secure transaction environment. Following these guidelines is crucial for avoiding potential issues and maximizing the benefits of First Bank's code transfer system.

The subsequent section will explore the different types of code transfers available and their respective benefits.

Conclusion

This article explored the multifaceted process of First Bank code transfers, highlighting the crucial elements of security, efficiency, and user experience. Key aspects examined included authentication mechanisms, security protocols, account access controls, transaction initiation, funds availability, code generation, confirmation procedures, and robust error handling. The intricate interplay of these components underscores the significance of a well-structured system for secure and reliable financial transactions. The system's ability to validate user identity, secure data transmission, and accurately reflect funds availability forms the cornerstone of trust within the financial ecosystem.

The implementation of robust security measures, encompassing encryption, multi-factor authentication, and regular security audits, demonstrates a commitment to safeguarding customer assets. This proactive approach is essential in mitigating risks associated with financial fraud and ensuring the integrity of transactions. As technology evolves, the ongoing refinement and adaptation of these security protocols remain paramount. Maintaining public trust in financial institutions hinges on the consistent application of these principles within the framework of code-based transfers. Ultimately, First Bank's code transfer system, with its emphasis on security and efficiency, reflects a commitment to providing dependable financial services. Continuous improvement and adaptation of security protocols to emerging threats is essential for maintaining the reliability and integrity of this critical banking function.

You Might Also Like

Blessed Friday Morning Images - Inspirational Good VibesTop Cowboy Surnames: A Western Heritage

Heartfelt Son's Death Anniversary Quotes & Messages

Famous Jones Celebrities: From A To Z

Luther Barnes Net Worth 2023: How Rich Is He?

Article Recommendations