A physical location of a financial institution, such as a bank, serves as a point of contact for initiating and managing direct deposit transactions. This includes opening accounts, completing paperwork for establishing direct deposit authorizations, and making any necessary adjustments to the setup. Customers can directly interact with bank staff for assistance with direct deposit, ensuring accuracy and compliance with established protocols. This interaction often involves presenting supporting documents.

Direct deposit, when facilitated through a branch, offers a tangible and reliable method of receiving funds. This is especially beneficial for individuals and businesses lacking or uncomfortable with online banking platforms. Direct deposit at a branch allows for immediate and personalized assistance, enabling resolution of any procedural questions or issues. The process remains a viable option for many, offering a physical interface for banking needs, including direct deposit. The historical prevalence of branch-based transactions, while less common now in comparison to online banking, remains an important aspect of financial accessibility for some demographics.

This discussion of branch-based direct deposit serves as a foundational element for understanding the broader context of payment processing methods. Moving forward, the article will delve into the advantages and disadvantages of branch-based transactions, alongside an exploration of alternative direct deposit methods.

What is Bank Branch for Direct Deposit

Bank branches play a crucial role in facilitating direct deposit transactions. Understanding their function is essential for navigating financial processes effectively.

- Location

- Service

- Documentation

- Assistance

- Security

- Accessibility

A bank branch's location provides a physical point of service for direct deposit. The service offered encompasses initiating and managing direct deposits, including account opening and adjustments. Documentation is critical; customers may require forms for setup. Bank staff offer assistance, crucial for guiding clients through the process. This face-to-face interaction enhances the security and reliability of the transaction. Branch accessibility remains a valuable option for individuals, particularly those who lack the digital resources or confidence in online banking. For example, a person without internet access might rely on a branch to set up their payroll direct deposit.

1. Location

The geographical location of a bank branch is intrinsically linked to the function of facilitating direct deposit. A branch's physical presence provides a crucial element for individuals who may prefer or require in-person interactions. Accessibility is paramount; a branch strategically situated within a community's reach enables direct deposit services for those who may lack the technical skills or confidence in online banking. This is particularly vital in areas with limited digital literacy or infrequent internet access. Individuals relying on direct deposit for crucial funds, such as payroll or government assistance, benefit from the availability of a nearby physical location for account setup and transaction resolution.

Consider a rural community with limited internet access. A local branch, acting as a vital hub, simplifies the direct deposit process for residents receiving social security payments or agricultural subsidies. This direct engagement empowers individuals and facilitates smoother financial transactions compared to solely relying on online platforms. Conversely, in metropolitan areas with extensive online banking infrastructure, branches still maintain value for complex direct deposit needs or urgent issues. A branch's location, in conjunction with other factors, thus determines its utility in the direct deposit landscape.

Understanding the critical role of location in a bank branch's ability to facilitate direct deposit highlights the multifaceted nature of financial service provision. The physical presence of a branch remains a tangible and reliable resource, especially for those who might not be able to fully utilize online alternatives. This understanding underscores the significance of balancing digital accessibility with the continued practical importance of physical locations, emphasizing the diversity of needs within a broader financial ecosystem.

2. Service

A bank branch's service offerings are integral to its function in direct deposit. This service encompasses the facilitation of direct deposit transactions, encompassing account setup, authorization procedures, and resolving any ensuing issues. Effective service is crucial for ensuring smooth and secure direct deposit processes. Without adequate service, difficulties can arise, leading to delays or errors in the delivery of funds. Reliable service, conversely, bolsters the security and efficiency of financial transactions.

Real-life examples illustrate this. A customer experiencing payroll direct deposit issues might require in-person assistance from a branch representative. This interaction would involve troubleshooting the problem, possibly correcting a registration error or updating account details, ensuring funds are received without delay. Similarly, a small business owner needing to set up a direct deposit for regular vendor payments requires specialized assistance, demonstrating a crucial need for dedicated service personnel within a branch. The expertise offered at a branch ensures compliance with direct deposit protocols and avoids costly processing errors. In essence, effective service within a branch translates to a reliable and secure process for direct deposit.

The understanding of service's role within the context of bank branches for direct deposit highlights the importance of qualified personnel and streamlined processes. The efficiency and security of direct deposit are dependent on this service component. Furthermore, the quality of service provided directly influences customer satisfaction and trust in financial institutions, underpinning the vital link between branch operations and overall financial health. This underlines the continued importance of accessible and competent service provision within the context of increasingly digitized financial systems, where a branch's role remains crucial for certain customers and transactions.

3. Documentation

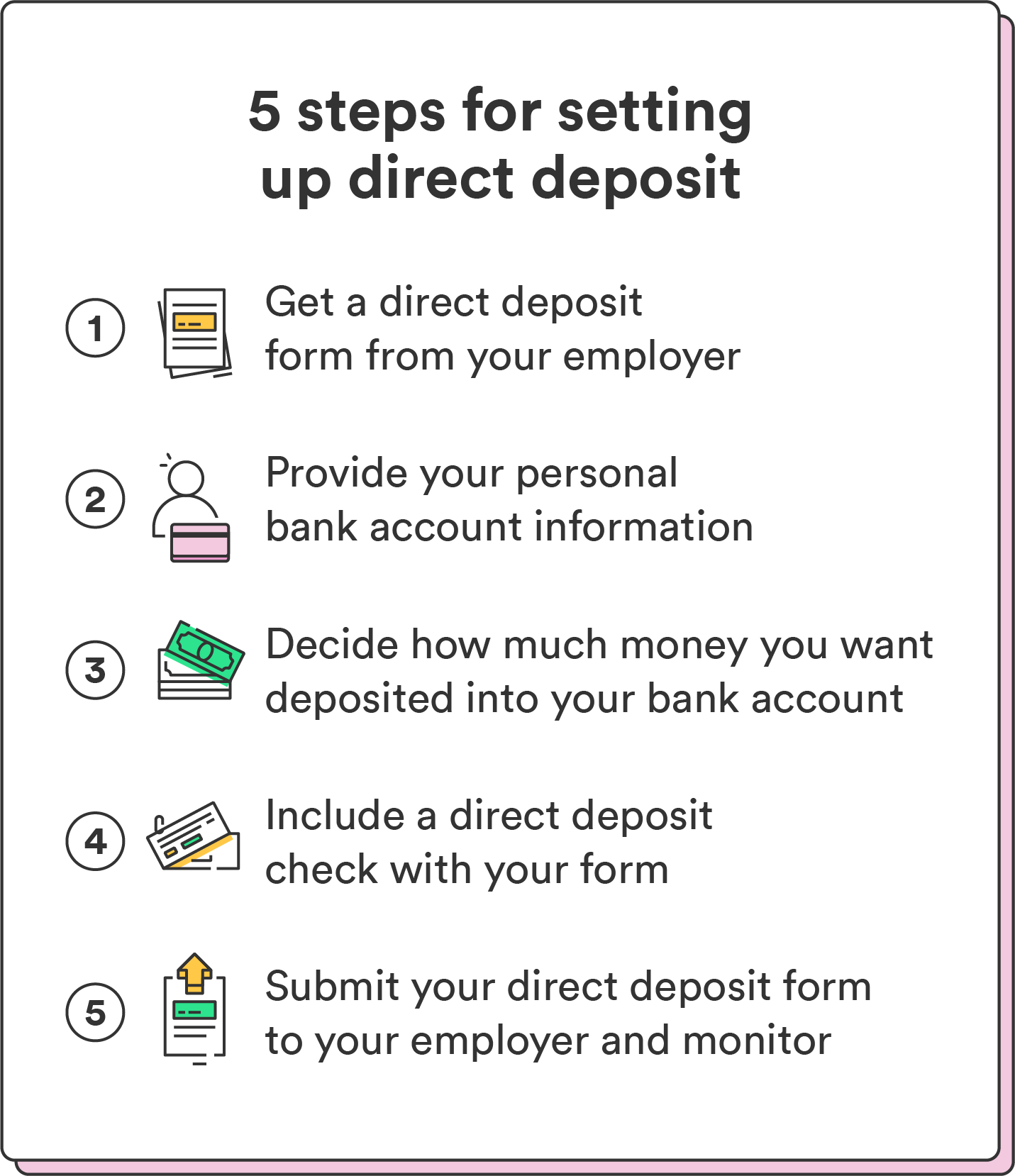

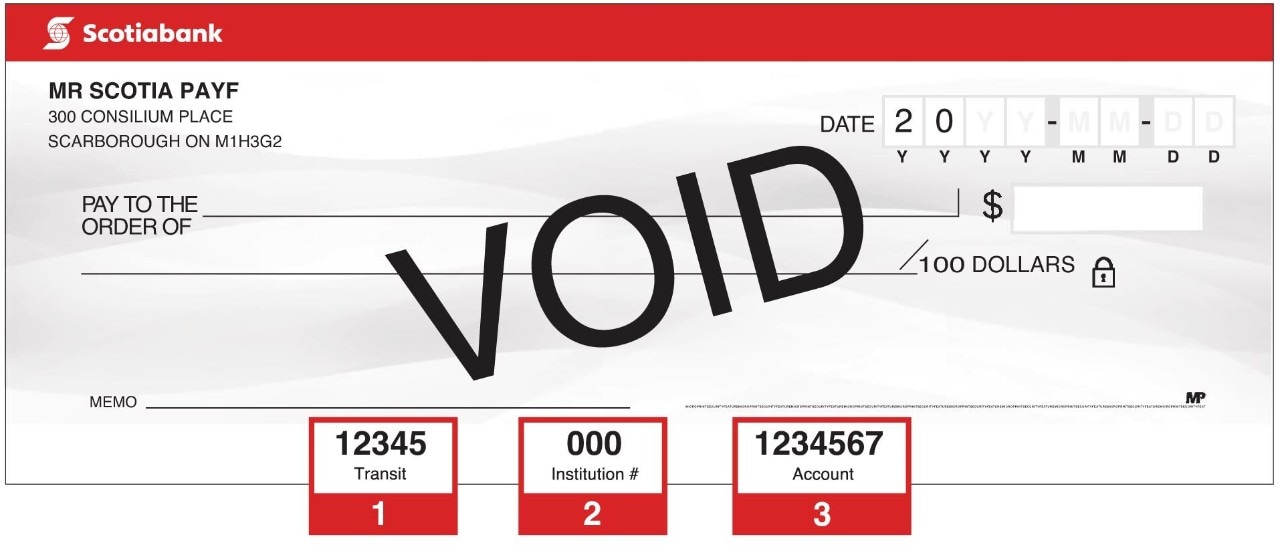

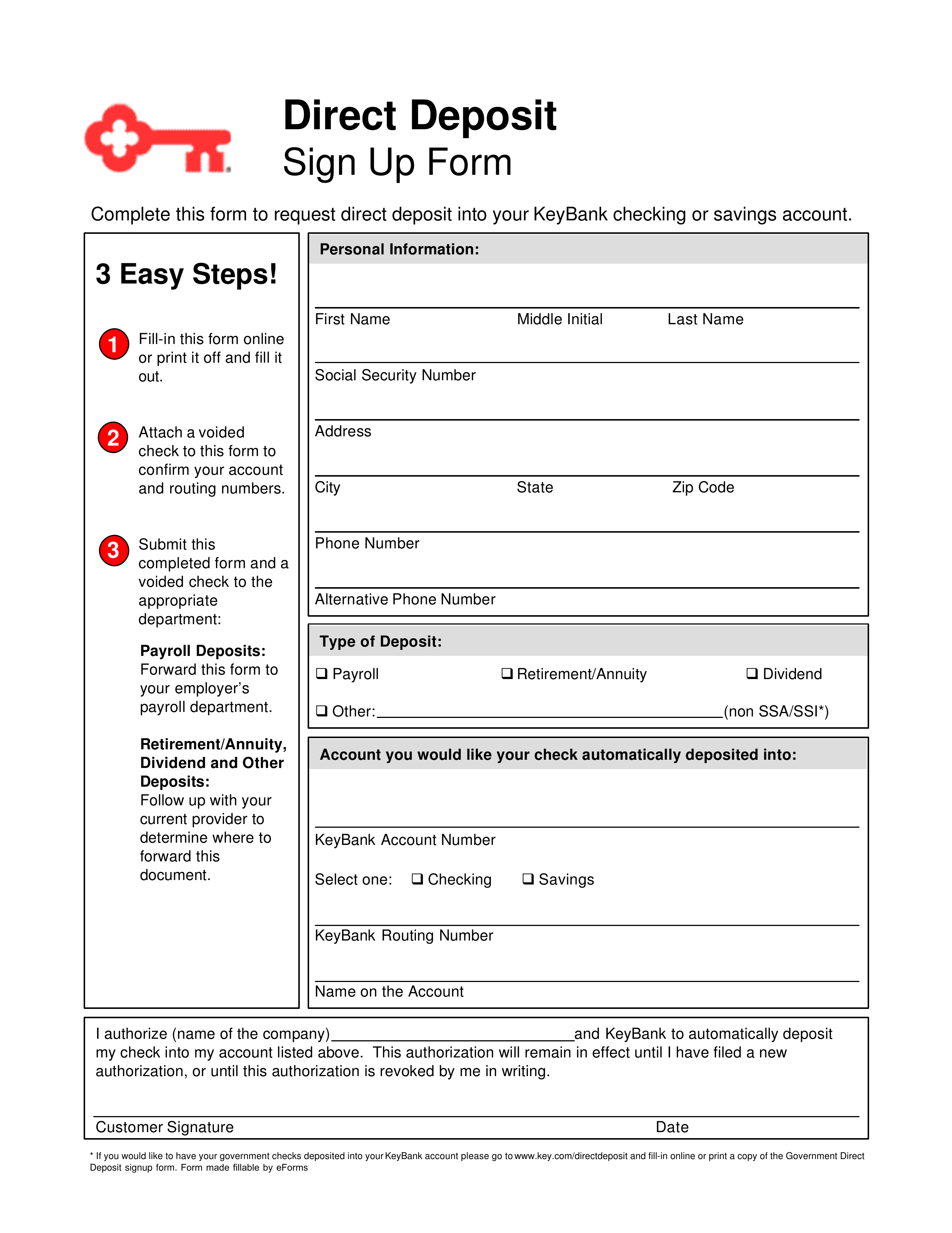

Documentation is inextricably linked to the function of a bank branch in facilitating direct deposit. Accurate and complete documentation is fundamental to establishing direct deposit authorizations. This encompasses the necessary forms, supporting identification, and confirmation of account details. The physical presence of a branch allows for the secure handling and validation of these documents. Without proper documentation, a bank cannot process a direct deposit request correctly, leading to potential delays, errors, or security breaches.

Consider a scenario where an individual seeks to initiate payroll direct deposit. The branch requires specific forms, including authorization slips and government-issued identification. This documentation serves as evidence of the individual's identity and their intent to receive funds via direct deposit. Without these documents, the transaction cannot proceed. Similarly, for businesses setting up direct deposit for vendor payments, the bank requires detailed information regarding the business and the recipient's accounts, alongside legally sound authorization forms. This thorough documentation ensures compliance with regulations and safeguards against fraud. The accuracy and completeness of documentation directly impact the efficiency and security of the direct deposit process. The physical act of presenting and verifying these documents within a branch setting provides a tangible security measure.

The importance of documentation within a bank branch for direct deposit is underscored by its role in preventing errors and ensuring compliance. The presence of comprehensive documentation creates a verifiable audit trail, essential for resolving disputes or investigating irregularities. Thorough documentation also aids in fraud prevention. By requiring explicit authorization and confirmation, the branch minimizes the risk of unauthorized access to accounts or fraudulent direct deposit attempts. The ability to meticulously document each step of the direct deposit process enhances the overall security and reliability of financial transactions, emphasizing the crucial role of accurate paperwork in maintaining the integrity of the financial system. Ultimately, a deep understanding of the documentation requirements associated with direct deposit is essential for both individuals and financial institutions.

4. Assistance

Assistance provided by bank branch staff is a critical component of direct deposit services. The ability to offer personalized guidance and support directly impacts the successful execution and security of these transactions. Direct deposit procedures can be complex, involving multiple steps and potentially intricate account configurations. Branch staff expertise in navigating these procedures is essential for clients. Without adequate support, individuals and businesses might experience delays, errors, or security vulnerabilities in establishing or maintaining direct deposit authorizations.

Real-world scenarios highlight the significance of this assistance. A customer experiencing payroll direct deposit issues might require in-person guidance from a branch representative to identify and correct registration errors or update account details. This personalized assistance ensures that funds are received promptly and accurately. Similarly, a small business owner setting up a direct deposit system for vendor payments necessitates specialized assistance. Dedicated branch staff can ensure the process complies with relevant regulations and avoids potential financial complications. The presence of trained personnel to address specific questions and concerns is integral to smooth transactions.

Understanding the link between assistance and direct deposit transactions underscores the enduring value of bank branches in a world increasingly reliant on digital financial services. While online platforms offer certain functionalities, the human element of personalized support remains a critical aspect of direct deposit success for many customers. This crucial understanding emphasizes the continuing need for skilled personnel within bank branches, particularly for individuals or businesses navigating complex direct deposit requirements or experiencing technical difficulties. Consequently, well-trained, approachable staff play a crucial role in mitigating potential errors and promoting customer confidence in the direct deposit process.

5. Security

Security is paramount in direct deposit transactions, particularly when facilitated through a bank branch. The physical presence of a branch offers a tangible layer of protection against potential threats and errors, distinct from entirely online processes. Maintaining secure handling of sensitive financial data is critical for both individuals and institutions. This section examines key facets of security within the branch-based direct deposit context.

- Physical Security Measures

Bank branches often incorporate robust physical security measures, including security personnel, surveillance systems, and controlled access. These safeguards deter theft and unauthorized access to sensitive financial documents, including direct deposit authorizations and account information. Secure facilities reduce the risk of physical breaches, ensuring the safety of sensitive information, which is paramount in direct deposit. This tangible presence acts as a deterrent, impacting the overall security perception associated with in-person transactions.

- Personnel Training and Protocols

Thorough training and adherence to established protocols for staff handling direct deposit transactions are crucial. Employees need comprehensive knowledge of security procedures, including verification processes for individuals and documents. Maintaining up-to-date security procedures within the branch minimizes risks associated with human error, misrepresentation, or fraudulent attempts. This detailed training is essential, impacting security for both the financial institution and its customers.

- Data Protection and Confidentiality

Bank branches are obligated to safeguard customer data. Physical security measures, combined with adherence to regulations and data encryption, protect sensitive information related to direct deposit transactions. These measures reduce the chance of data breaches, crucial for maintaining customer trust and safeguarding financial information. Confidentiality is vital in the handling of direct deposit data, whether in paper or electronic form.

- Fraud Detection and Prevention

Branch staff play a vital role in detecting and preventing potential fraudulent activities related to direct deposit. Procedures for verifying identities, scrutinizing documentation, and recognizing suspicious patterns are essential safeguards. This proactive approach contributes significantly to the security of transactions. Detection and prevention strategies are implemented to maintain trust and mitigate potential financial harm. Implementing these strategies at the branch level adds a critical layer of protection.

In conclusion, the security of a direct deposit transaction through a bank branch hinges on a combination of physical safeguards, comprehensive employee training, rigorous data protection protocols, and a commitment to fraud detection. The physical presence of a branch allows for a layer of security that complements online methods, enhancing the overall confidence and trust associated with such financial processes.

6. Accessibility

Accessibility in the context of bank branches for direct deposit is a multifaceted concept encompassing physical location, service availability, and digital literacy considerations. The accessibility of a branch directly affects the ability of individuals and businesses to utilize direct deposit services. A readily available branch in a community improves access to this crucial financial service.

The physical location of a bank branch is a fundamental element of accessibility. A branch strategically situated within a community's reach facilitates direct deposit services for those who lack the technical proficiency or comfort using online banking. For populations with limited digital literacy or infrequent internet access, a nearby branch can simplify direct deposit, making it easier to receive vital funds such as payroll, government assistance, or social security payments. This is especially important in rural areas, where access to online banking might be limited. A branch's physical presence enables a tangible form of financial inclusion for these communities.

Beyond physical proximity, accessibility also extends to the services provided within the branch. Clear signage, user-friendly layout, and well-trained staff are essential components. Individuals with disabilities or those requiring assistance might encounter barriers in less accessible branches. Conversely, a branch with comprehensive support services, including multilingual staff and readily available assistance for non-technical users, improves accessibility. For example, a branch dedicated to serving a population with limited English proficiency ensures inclusivity and proper support for direct deposit transactions, which are critical for their economic well-being. Thus, service accessibility fosters convenience and simplifies the financial process.

The understanding of accessibility within the context of bank branches for direct deposit highlights the interplay of physical location, service quality, and digital literacy. The ability to utilize direct deposit services directly impacts financial security and independence. Accessible branches ensure that diverse communities can effectively participate in the modern financial system. This broader perspective underscores the importance of understanding and addressing the various needs of diverse communities to achieve comprehensive financial accessibility. Consequently, financial institutions must strive to implement strategies that ensure the accessibility of direct deposit services through their branch networks.

Frequently Asked Questions about Bank Branches for Direct Deposit

This section addresses common inquiries regarding the role of bank branches in direct deposit transactions. Understanding these points clarifies the process and its implications.

Question 1: What is the purpose of a bank branch in facilitating direct deposit?

A bank branch serves as a physical location for individuals and businesses to initiate, manage, and resolve issues related to direct deposit. This includes setting up direct deposit authorizations, updating account information, and providing assistance with any associated problems.

Question 2: Are bank branches still relevant for direct deposit in the digital age?

Yes. While online banking is prevalent, bank branches remain essential for customers who prefer in-person assistance, lack digital literacy, or require immediate resolution for complex issues. Branches provide a valuable point of contact for troubleshooting problems that might not be easily addressed online.

Question 3: How does a bank branch ensure the security of direct deposit transactions?

Security measures employed by bank branches include physical security protocols, trained personnel, and adherence to strict security guidelines for handling sensitive financial data. These methods reduce the risk of errors, fraud, and data breaches during direct deposit transactions.

Question 4: What documentation is needed at a bank branch for setting up direct deposit?

Required documentation varies by institution but generally includes valid identification, account details, and formal authorization forms specifying the source and destination of funds for the direct deposit.

Question 5: Can I use a bank branch for direct deposit if I am not a customer of that institution?

Generally, no. Most institutions require that the account receiving the funds be maintained at the branch in question or another account authorized by the branch. There are typically restrictions on facilitating direct deposits for non-customers.

Question 6: What are the potential advantages and disadvantages of using a bank branch for direct deposit?

Advantages include in-person assistance for complex issues and tangible security measures. Disadvantages might include limited hours and potential wait times, although this can depend greatly on the branch location and service demands.

In summary, bank branches continue to play a vital role in facilitating direct deposit, particularly for individuals and businesses seeking in-person support, security, and resolution of specific issues. The availability and accessibility of these physical locations should not be underestimated. This ensures confidence in the security and efficacy of direct deposit processes.

This concludes the FAQ section. The subsequent section will delve into the practical implications of different direct deposit methods.

Tips for Utilizing Bank Branches for Direct Deposit

Effective use of bank branches for direct deposit transactions requires careful planning and understanding of procedures. Following these tips can streamline the process and minimize potential issues.

Tip 1: Plan Ahead. Schedule a visit to the branch during operating hours, considering potential wait times, especially during peak periods. Advance planning minimizes disruptions to workflow and allows ample time for processing. This proactive approach ensures a smoother interaction and reduces the likelihood of unexpected delays.

Tip 2: Gather Required Documents. Compile all necessary identification, account details, and any forms required for direct deposit authorization. This preparation ensures a swift and accurate transaction process. Thorough documentation is crucial for verification and compliance.

Tip 3: Know the Branch's Procedures. Familiarize oneself with the specific procedures for direct deposit at the chosen branch. This includes understanding the necessary forms, required supporting documentation, and any specific instructions or requirements. Thorough knowledge mitigates potential errors and facilitates a smooth experience.

Tip 4: Seek Assistance When Needed. If encountering any difficulty or uncertainty in the direct deposit process, promptly seek assistance from branch personnel. This proactive step ensures accuracy and prevents potential issues. Staff are trained to provide support and clarify any doubts or concerns.

Tip 5: Verify Information. After completing the direct deposit setup, double-check all details and confirmation documents for accuracy. Confirm all account information, authorization details, and any other relevant aspects. This verification minimizes the risk of errors and ensures the intended funds are deposited in the correct account.

Tip 6: Maintain Records. Keep copies of all completed forms, authorization documents, and confirmation receipts. This record-keeping is essential for future reference. This meticulous documentation aids in resolving any potential disputes or inquiries.

Tip 7: Address Issues Promptly. If any issues arise after setting up direct deposit, contact the branch for prompt resolution. Diligent communication and timely follow-up are key. This proactive approach minimizes disruptions and potential complications.

By adhering to these tips, individuals can effectively leverage the services offered at bank branches for direct deposit transactions. This approach ensures a smooth, secure, and accurate financial process, optimizing the benefits associated with this method.

The next section will delve into the advantages and disadvantages of different direct deposit methods, alongside a comparison of online and branch-based options.

Conclusion

This exploration of bank branches in the context of direct deposit highlights the enduring relevance of physical locations within the modern financial landscape. Direct deposit, facilitated through branches, offers a tangible and reliable method for receiving funds. The process, while perhaps less prevalent than online options, retains significant value for individuals and businesses, especially those requiring personalized assistance, secure document handling, or specialized guidance. Key aspects, such as the physical presence for verification, the provision of personalized support, and the security measures inherent in branch-based transactions, underscore the continued importance of physical banking facilities. This traditional approach provides a crucial alternative and safeguard within the broader spectrum of financial service delivery.

The continued availability and accessibility of bank branches, particularly in communities with limited digital literacy or access to technology, ensure equitable access to vital financial services. Maintaining a robust branch network alongside innovative digital solutions ensures a complete and comprehensive approach to financial inclusion. The exploration of "what is bank branch for direct deposit" thus demonstrates the enduring need for a multifaceted approach to financial service provision, recognizing the diverse needs and preferences of the public within contemporary financial systems.

You Might Also Like

Christian Carino Net Worth 2024: UnveiledNational Geographics: Worth It? Exploring Value

Bill Hemmer & Sandra Smith: News & Analysis

Legendary John Claude Van Damme: Action Star & More

Coolest Ice: Ice Ice Baby!

Article Recommendations